Get in touch

If you have any questions relating to this article or have any employment issues you would like to discuss, please contact the Employment team on [email protected]

Today (24 September 2020), the Chancellor announced new plans to support jobs following new covid-19 restrictions announced by the Prime Minister. A new Job Support Scheme (JSS) has been announced which will commence from 1 November 2020 following the end of the Coronavirus Job Retention Scheme (JRS) and Flexible Furlough Scheme (FFS) on 31 October 2020. The new JSS government wage subsidy scheme is designed to protect “viable jobs”, so for some employers difficult decisions will have to be made. Guidance has not been published but what do we know so far and how can employers prepare?

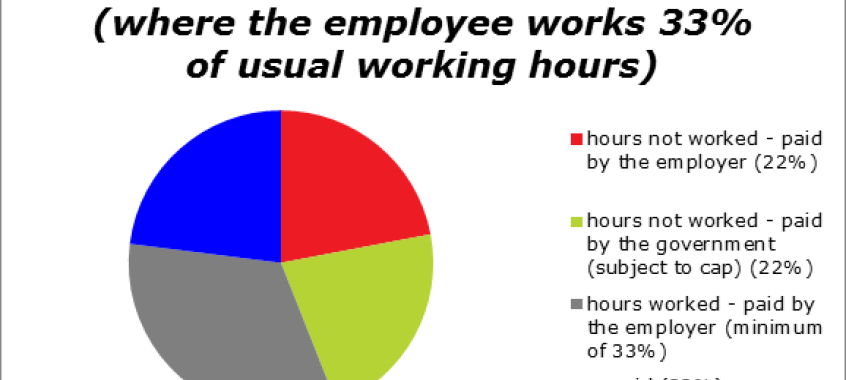

Under the terms of the JSS, where an employee is able to work but because of government restrictions/covid-19, their employer can only offer part time work, the employer will continue to pay the employee’s “usual wages” for those part-time hours and for the hours not worked, both the government and the employer will each pay one third, subject to a government cap of £697.92 a month.

The JSS ensures that employees will earn at least a minimum of 77% of their usual wages, where the government contribution has not been capped.

Yes, for the first 3 months of the scheme, an employee must work at least 33% of the usual working hours. It is expected that the government will review this percentage after the first 3 months.

The key difference between the JSS and the JRS is that employees must NOT be made redundant or be subject to any redundancy notice during the period for which the employer is claiming the JSS. The employee’s role must be viable, which means employers may have to make some difficult decisions about roles moving forward.

There are payroll date requirements too - employees are only eligible under the JSS is they are on their employer’s PAYE payroll on or before 23 September 2020. This means a Real Time Information (RTI) submission notifying payment to that employee to HMRC must have been made on or before 23 September 2020.

Neither the employer nor the employee needs to have previously used the JRS.

The JSS is available to all employers who have a UK bank account and are registered for PAYE. However, the JSS is specifically aimed at small and medium-sized enterprises (SMEs). For larger employers, the JSS can still be accessed but these employers will need to show that their business has been impacted and that their turnover has fallen by a third. There will be a Financial Assessment Test for large employers. Also, it is expected large employers would not pay dividends to shareholders while using the scheme.

Working hours can vary but must be fixed for a minimum period of 7 days. Although working hours can vary, they cannot drop lower than 33% of normal working hours.

If hours worked are more than 33% then then proportion of unpaid hours and government support will also vary, subject always to the cap and the employee could in fact earn more, the more they work. So, if the employee works 50% of normal hours, the employer would pay 67% and the government 17%, meaning the employee would receive 83% of their normal pay. If instead, the employee works 70% of their usual hours, the employer pays 80%, the state 10%, with the employee receiving 90% of usual pay (if you round all the % up).

Employees can also “cycle on and off” of the scheme, so employees could go back to full time working for 3 weeks; for example, before dropping back to 33% for a week.

Employers would use the method that was used to calculate pay/hours under the JRS. Please note that employers should use an employee’s pre-furlough rate of pay when calculating support under the JSS if the employee is currently on JRS.

Receiving support under the JSS necessitates changing an employee’s contractual working hours and pay; effectively the employee is being placed on a short-time working arrangement. Similar to the JRS, employers must agree the new working arrangements and pay with their employees and any changes must be agreed in writing. The written note of the change may also be requested by HMRC.

As well as contractual obligations, employers should also remember that obligations relating to discrimination in how they select employees to be subject to the JSS.

The current government fact sheet says it is not expected this will happen.

The JSS grant from the government does not cover either Class 1 employer NICs or minimum auto enrolment pension contributions; however, employers will be responsible for these payments in respect of the proportion they are responsible for . All payments paid to the employee are subject to usual deductions for income tax and employee NICs.

The JSS will run for six months from 1 November.

Employers will be able to make a claim online through Gov.uk from December 2020. JSS will be paid on a monthly basis in arrears. Employees should be paid first and in full (e.g. 77%) and that payment should be reported to HMRC via an RTI return.

The JSS is designed to work with the government’s Job Retention Bonus. Under this scheme, businesses receive a one-off payment of £1,000 for every previously furloughed employee they still employ at the end of January 2021.

The new rules are complicated, particularly where the employee works more than the minimum 33% of hours and could cost the employer more. Employers should review their workforces, pipelines and customer demand and make some difficult decisions. If it is unlikely that a role will be “viable”, then employers should remember their legal requirements under redundancy – and potentially collective redundancy – rules and take advice.

There are also other issues we await clarification on, particularly around NICs and pension contributions, although the employer should expect to pay these for the proportion of worked/unworked hours they are responsible for.

The proportion of wages paid (or unpaid) under the JSS where the employee works a minimum of 33% can be illustrated as follows:

Consistent with our policy when giving comment and advice on a non-specific basis, we cannot assume legal responsibility for the accuracy of any particular statement. In the case of specific problems we recommend that professional advice be sought.

Share:

If you have any questions relating to this article or have any employment issues you would like to discuss, please contact the Employment team on [email protected]

Sign up to receive the latest news on areas of interest to you. We can tailor the information we send to you.

Sign up to our newsletter